The holiday season marks the point in the calendar where I start to think about my "what to expect next year" piece.

It is a time for me to reflect on the past year’s uncertainties, how we navigated them, and learning opportunities for us to improve upon. Before we delve into 2023 predictions, it’s always helpful to understand where we were at the beginning of the year and what our expectations were at that time.

We began 2022 with the expectation that economic growth would be weaker than most investors anticipated and while inflation would fall, it would do so at a slower pace than expected due to a persistence of shortages and as wage growth increased. In addition, we expected the U.S. would fare worse than other developed markets due to its large weights in sectors where expectations and valuations were most excessive (i.e., high-growth stocks). On bonds, we expected to see long-term bond yields rise across most major economies, especially in the U.S., where we observed that inflationary pressures were particularly strong. In our January commentary, we stated that the U.S. Federal Reserve (Fed) and the Bank of Canada would have to raise interest rates to levels that we haven’t seen in decades, and we expected rates to be kept at those levels for some time. As a result, higher bond yields would weigh heavily on both fixed income and equities.

So how did we fare? At the time of this writing, global equities are down -15.95% in Canadian dollar terms, while U.S. equities are down -16.05%. As we predicted, growth equities have significantly underperformed the broad indices, especially in the U.S. where they are down -26.15%. There were few safe havens to be found in 2022 as both bonds and equities became positively correlated. However, value- and energy-focused strategies managed to avoid the brunt of the downturn. In our portfolios, we tilted in the direction of the Value Factor and/or Canadian equities, capitalizing on those themes. In our Counsel Strategic Portfolios over the last three years, we’ve built up a significant core position within the multi-factor strategies that have contributed significantly to driving both absolute and risk-adjusted returns.

So far, so good, but what did we miss? A couple of things stand out. While our expectations were largely correct, in hindsight, we could have been more aggressive in reducing risk exposure across equities and bonds in favour of short-term fixed income. In addition, our expectation that global real estate assets would be more resilient and provide a buffer to inflation and equity market weakness did not stand up. The only consolation is that global real estate did no worse than global equities.

One of the most important lessons for 2022 is that the financial markets are vulnerable to a sudden shock after a decade of interest rates being artificially below the nominal growth rate of GDP.

This led to years of yield chasing, weak underwriting standards, rising leverage, and rampant speculation in high- growth stocks, illiquid securities, crypto-currencies, and volatility strategies (just to name a few)[1]. We had two shocks to the financial system over the last three years: the Covid crash of 2020 and the rapid rise of interest rates of 2022. The “pre-existing conditions”, to use a medical term, rendered the financial system extremely fragile, which should be of no surprise to investors. We have pointed many times over the years that investor expectations have become disconnected from historic norms. We were not alone in this view. In 2019, Mervyn King, the former Governor of the Bank of England, gave a speech in which he pointed out that global debt relative to GDP was much higher than in 2008. This high level of debt and depressed level of growth could not be solved by monetary policy, it only papered over the cracks. Lord King concluded that we were sleepwalking toward another crisis. Little did he know what was to come. His talk was entitled “The World Turned Upside Down,” and it’s worth a listen.

Market Expectations for 2023

Looking forward, we believe that what happens in 2023 will be determined by the answers to these three questions:

- Will the world's major economies fall into recession?

- Will inflation recede?

- How far will central banks raise interest rates?

On the question of recessions, Nobel Laureate Paul Samuelson remarked that stock markets have predicted nine out of the past five recessions. In contrast to the markets, we’ve rarely forecast recessions. This is partly because the usual situation is for economies to grow. Recessions tend to occur once every decade or so. Accordingly, anyone forecasting a recession is betting against the norm and the odds of being proven wrong are high.

I mention all this as background to saying that we are expecting recessions in the U.S., Canada, and in Europe next year. Admittedly, the recent hard activity data have been more resilient than we had anticipated. But the survey data, including the Purchasing Managers’ Indices, are now consistent with falling output in the euro-zone and a marked slowdown in growth in the U.S. and Canada. And, there are good reasons to think that aggregate demand, and therefore economic growth, will be squeezed further over the coming year.

Ordinary vs Extraordinary Recessions

The most obvious reason to expect demand to weaken is that the full effects of the substantial monetary tightening over the past 12 months have yet to be felt. This is just starting to hit interest rate sensitive sectors (notably housing) particularly hard. In addition to the effects of higher interest rates, economies in Europe are also having to contend with a large hit to their terms of trade, which will continue to weigh on incomes.

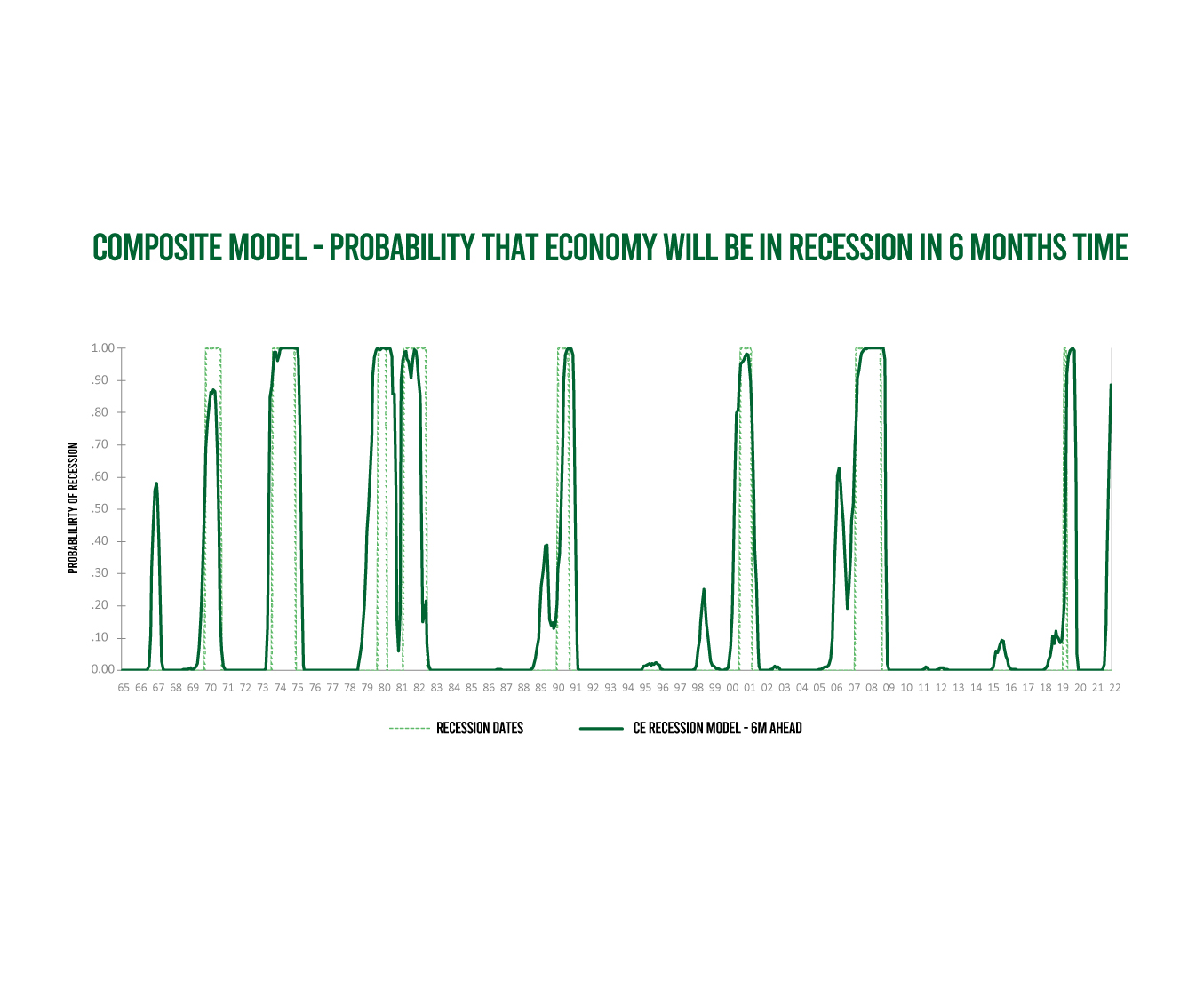

A proprietary recession indicator developed by Capital Economics now suggests there is a 90% probability that the U.S. will be in recession in six months time. It has never been this high without a recession following. When your macro views and the proprietary models that you follow are telling you the same thing, it's wise not to ignore them.

Probability of a Recession in Six Months

Source: Capital Economics

With that said, it's important to stress that, in the case of Canada and the U.S. at least, we anticipate a relatively mild recession. The adverse hit to the terms of trade means that recessions in Europe will be deeper. But, even here, the contraction in Gross Domestic Product (GDP) will be much smaller than the Global Financial Crisis (2007-2009) and Pandemic (2020) recessions. What's more, a recovery is likely to commence over the second half of next year.

Our perceptions are naturally framed by recent experience, but when it comes to recessions the past two have been extraordinary: the recession in 2007-09 was caused by the largest financial crisis since the Great Depression in the 1930s, and the recession of 2020 was caused by a pandemic that shut down the global economy. In contrast, the anticipated recession in 2023 is likely to be less extreme - perhaps somewhat like the 2001 recession. This is not to minimize the significance of the looming downturn, or the pain that will be inflicted on households and small businesses, but rather to underscore the importance of not viewing the next recession through the lens of the last one.

Better News Coming on Inflation

All of this adds up to a gloomy economic backdrop. If 2023 is to bring better news, the chances are it is likely to come on the inflation front. There is already substantial evidence that inflation is slowing as shortages ease. Forward-looking indicators suggest that this is likely to continue through the course of the next year. China's slowdown will be a source of global disinflation and, while energy prices will remain elevated, energy inflation should slow.

There remain bigger questions over the path of services inflation and non-core inflation (food and energy), which are governed to a much greater extent by the balance of supply and demand in economies. Admittedly, there were encouraging signs of a slowdown in services inflation in October's U.S. inflation data. But one month's data doesn't make a trend. And while some of the labour market surveys point to a further moderation in wage growth, they are still signalling growth rates that are inconsistent with the central bank's inflation targets.

We expect the picture should start to change over the course of next year as unemployment starts to rise across advanced economies, which will take the heat out of labour markets. We therefore expect core inflation to have moderated across developed markets by the end of 2023. The moderation will be more gradual in the euro-zone, where labour markets look especially tight. But the speed and extent to which headline and core inflation in Canada and the U.S. fall could be one of the surprise stories of 2023.

More Work for Central Banks

This brings us to the implications for monetary policy. The first point to make is that central banks across developed markets still have more work to do. This is particularly true of those in Europe, where core inflation will be slower to fall back, and the pace of policy tightening has so far lagged that in Canada and the U.S., particularly here at home where the Bank of Canada has seemingly signalled a pause with its December rate hike to 4.25%. Inflation looks likely to turn decisively lower next year. We think that the conditions will be in place for the Bank of Canada and the Fed to begin cutting interest rates, albeit at a gradual pace, by the final quarter of the year. Global equity markets, we believe, will make a new cyclical low by the spring of 2023 as the recession gets underway, rebounding to end next year higher than they are now.

Summary

If the past two years have taught us anything it is that shocks like Covid, the war in Ukraine, and so on, can appear from left field to upturn even the most deliberate forecasts. The effects of these shocks are still rippling through the global economy and mean that any forecasts for 2023 are subject to more uncertainty than usual. At the same time, new shocks may materialize: the rapid tightening of monetary conditions could expose financial vulnerabilities in unanticipated places, for example. Private debt vulnerabilities are building, and the fracturing of the global economy means that geo-politics has returned as a source of economic and financial risk are additional areas of concern.

And yet the potential for positive surprises exists too. Inflation could fall further than we anticipate, particularly in Europe, reducing the need for further monetary tightening. Meanwhile, the remaining Covid-era supply distortions could unwind faster and further than we expect, which would boost global production.

The one thing we can be reasonably sure about is that the economic backdrop is likely to look and feel very different in a year's time. Move the clock forward 12 months and our sense is that 2023 will have been a year of recession in advanced economies, continued weakness in China and falling inflation everywhere, particularly in Canada and the U.S. The prospect of a moderate recovery commencing in the second half and the Bank of Canada and the Fed cutting rates by the end of the year means there's light at the end of the tunnel. But as 2022 draws to a close, the tunnel still looks long.

Happy Holiday, wishing you and your loved ones a happy, healthy and prosperous 2023.

Corrado Tiralongo

Chief Investment Officer

Counsel Portfolio Services | IPC Private Wealth